The U.S. construction industry experienced a surge in demand in the years following the COVID-19 pandemic. The intense real estate market during the pandemic highlighted the shortage of housing stock across the United States. Between 2020 and 2022, private construction spending rose rapidly, fueled by a wave of new housing starts. In April 2022, housing starts reached their highest level in more than 15 years before declining to pre-pandemic levels as mortgage rates climbed. And just as private construction activity began to plateau, funding for public projects became available—most notably through the Bipartisan Infrastructure Law—driving growth in public-sector construction spending.

Today, however, the outlook for the construction industry is less certain amid economic headwinds, including a softening labor market, foreign import tariffs, and persistently high interest rates. Despite these challenges, construction firms continue to face severe labor shortages. The Associated Builders and Contractors, a leading industry trade group, estimated a shortfall of 439,000 workers. Meanwhile, the Bureau of Labor Statistics reported 306,000 openings for construction jobs as of July 2025.

In response to the labor shortage, the industry is increasingly drawing on a historically underrepresented segment of the population: women. Analyzing the newest data from the U.S. Census Bureau and the Bureau of Economic Analysis, researchers at Construction Coverage—a construction publication providing data and insights on workforce, wage, and industry trends—identified the best-paying states for women in the construction industry.

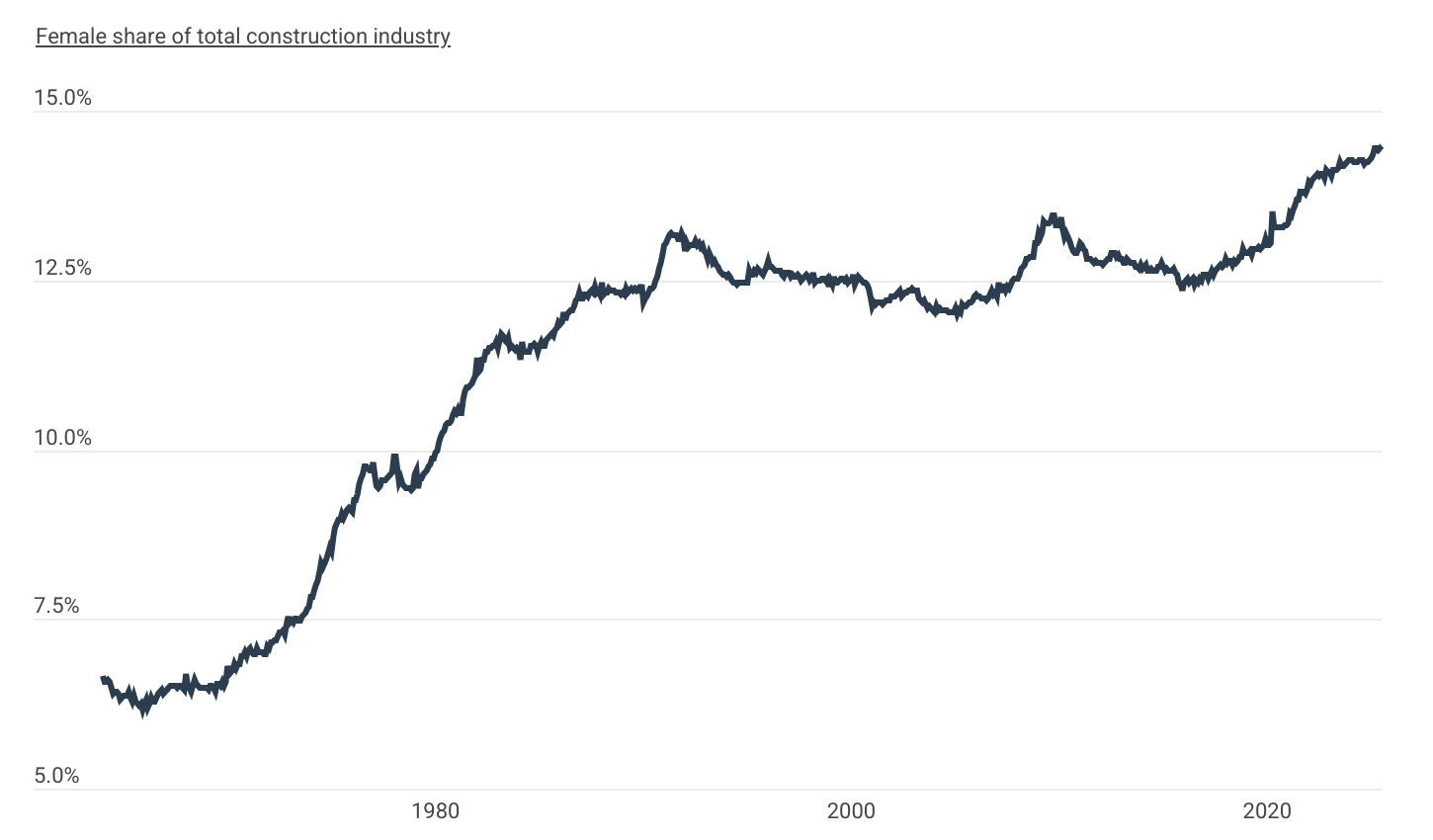

Female Employment in Construction

The share of women in construction employment has more than doubled since the 1960s and continues to rise

Source: Construction Coverage analysis of U.S. Bureau of Labor Statistics data | Image Credit: Construction Coverage

Construction has historically been a male-dominated sector. In the 1960s, only about 6% of construction industry workers were women. This figure began to rise sharply between 1970 and the early 1990s, coinciding with increasing rates of female labor force participation overall. Between then and the mid-2000s, female representation in the construction sector remained relatively steady, aside from some fluctuations during the Great Recession. However, since around 2016, the percentage of women in the construction industry has consistently increased. As of July 2025, 14.4% of all workers and 10.7% of full-time workers in the sector are women.

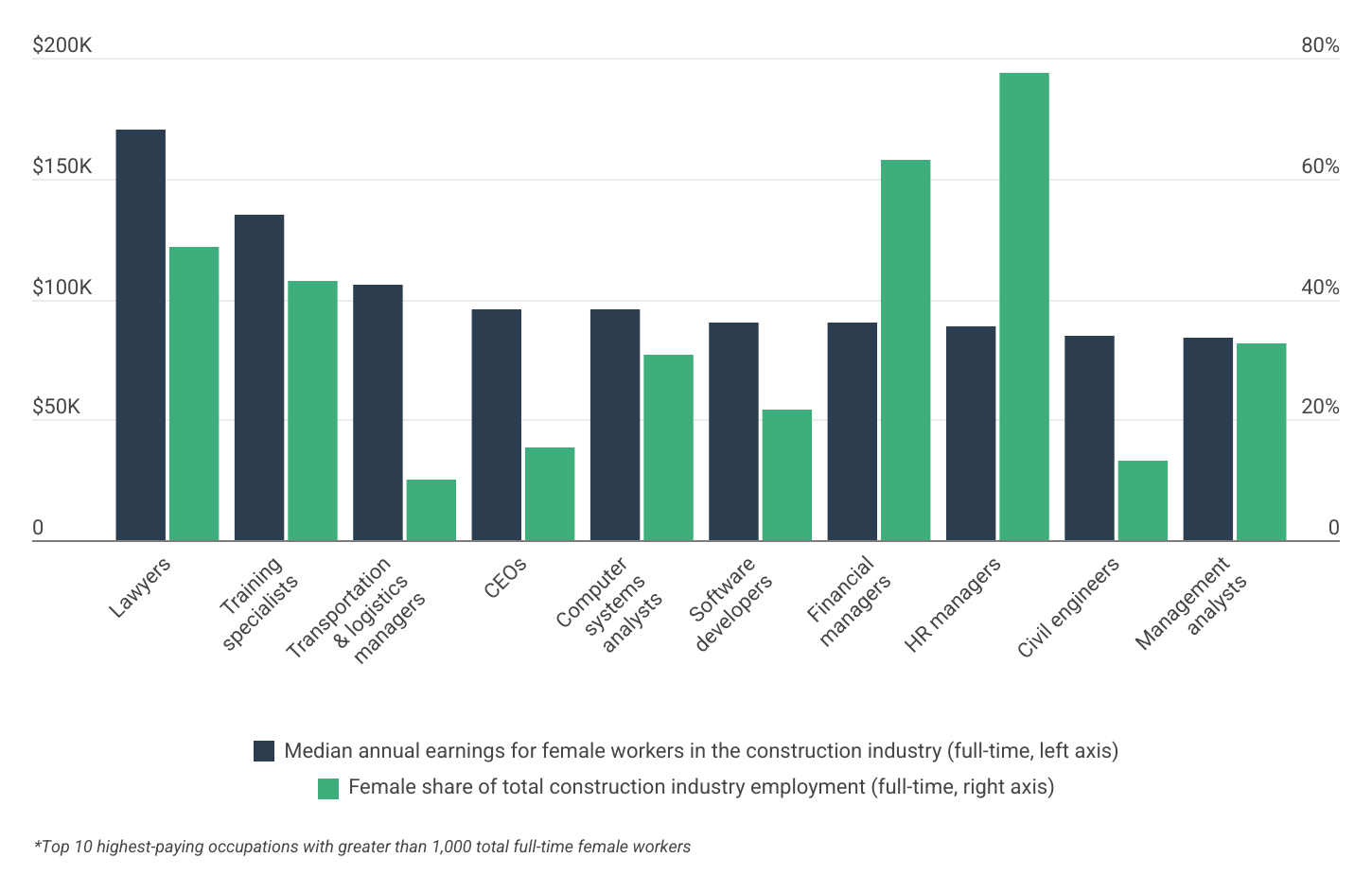

Top-Paying Occupations for Women in the Construction Industry

In the construction industry, women are disproportionately concentrated in high-paying jobs

Source: Construction Coverage analysis of U.S. Census Bureau data | Image Credit: Construction Coverage

While women still have low representation within construction trade occupations—such as plumbers, carpenters, masons, and electricians—they have disproportionately high representation in some of the industry’s best-paying jobs. For instance, lawyers in the construction sector are the industry’s top-paid workers, with median annual wages of $170,000 for female lawyers working full-time. Women account for more than 48% of construction industry attorneys, over four times higher than their overall representation in the sector. This trend is seen across many of the best-paying occupations for women in the construction sector, including training specialists, CEOs, computer systems analysts, software developers, financial managers, HR managers, civil engineers, and management analysts.

Due to women’s relatively high concentrations in the sector’s top-paying jobs, the median wage for full-time women working in construction exceeds that for all full-time working women in 39 states. Additionally, the gender wage gap in the construction industry is 4.9%, compared to 18.9% across all full-time workers.

Outside of occupation, location is a critical determinant of construction industry pay. Nationally, full-time female workers earn $54,044 annually in the sector, but pay varies widely by state. Additionally, regional differences in cost of living affect how far a given salary will go in a given location. To find the best-paying states, researchers at Construction Coverage analyzed data from the U.S. Census Bureau and the U.S. Bureau of Economic Analysis to rank states according to the median annual wage for full-time female workers in the construction industry, adjusted for cost-of-living differences.

Here is a summary of the data for Oregon:

Median annual wage for women in the construction industry (adjusted): $60,825

Median annual wage for women in the construction industry (actual): $63,697

Median annual wage for women in all occupations (actual): $56,093

Share of the construction industry that are women: 11.6%

For reference, here are the statistics for the entire United States:

Median annual wage for women in the construction industry (adjusted): N/A

Median annual wage for women in the construction industry (actual): $54,044

Median annual wage for women in all occupations (actual): $52,458

Share of the construction industry that are women: 10.7%

Commented

Sorry, there are no recent results for popular commented articles.