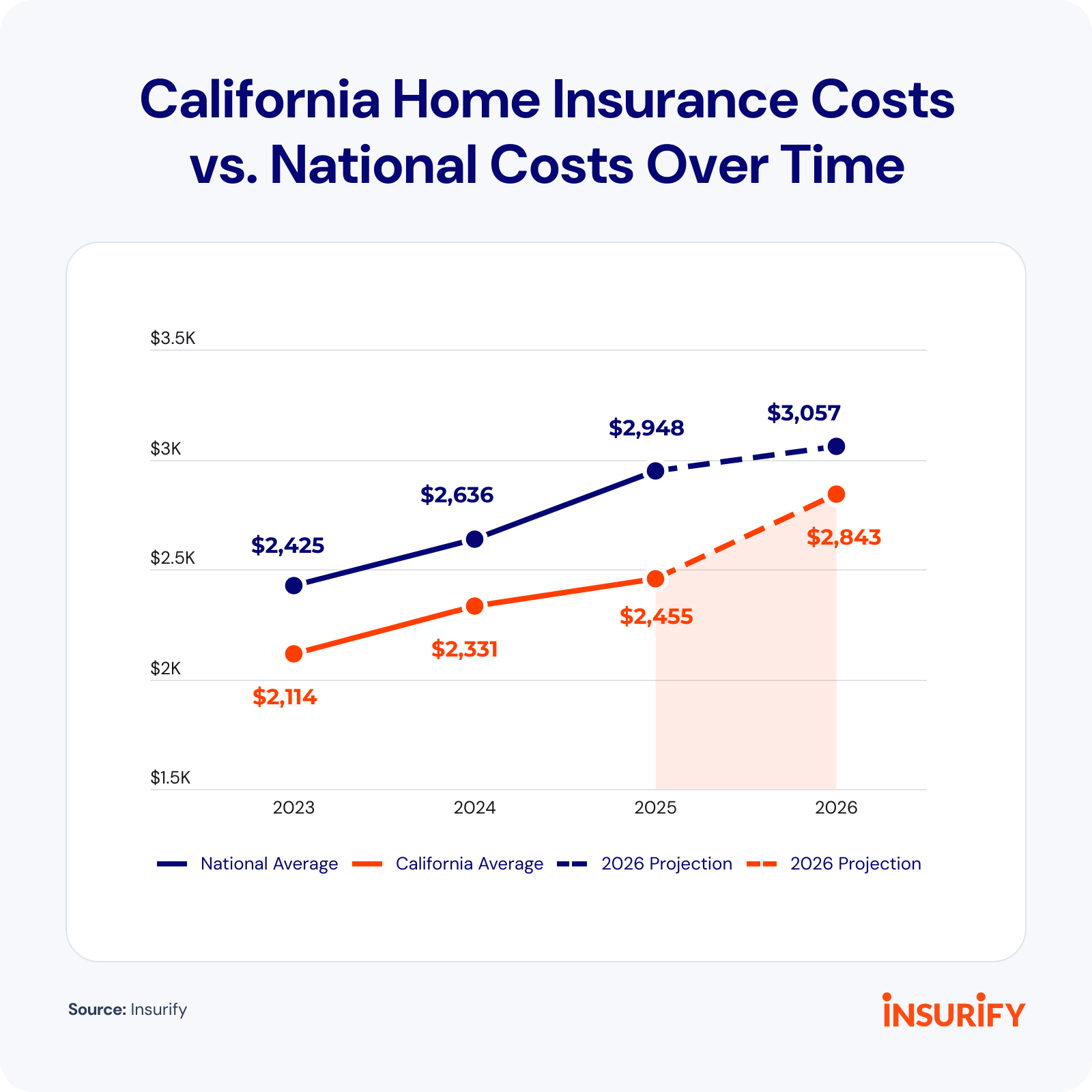

California’s home insurance costs have long been moderate, despite the state’s higher cost of living, largely because of its strict regulatory environment. Still, the average cost of homeowners insurance rose 5% in the Golden State last year, and an even higher increase could be on the way in 2026.

“In early 2025, the Palisades and Eaton fires upended the California home insurance market,” said Matt Brannon, senior economic analyst at Insurify and author of the 2026Insuring the American Homeowner Report. “In 2026, insurers will be looking to recoup their 2025 losses, which were significant, around $41 billion for the Los Angeles wildfires alone. They typically do that by increasing rates.”

Insurify data scientists also note that California insurers will likely begin using more advanced risk modeling to set rates in the state. As a result, Californians could see their home insurance rates increase 16% by the end of 2026, Insurify projects.

How California’s home insurance costs have changed over time

California requires insurance companies to submit to a rigorous review and approval process before they can implement rate increases. The strict regulatory environment has kept rates artificially low and contributed to California’s home insurance crisis, some experts say.

But in recent years, the California Department of Insurance (CDI) has approved some significant increases.

For example, State Farm requested — and received — an emergency rate increase following the early 2025 wildfires. As of early March 2026, the state and the insurer had reached an agreement for a 17% increase.

The settlement is before an administrative law judge for final approval.

In exchange for rate increases, however, the state has begun requiring insurers to sell more policies in high-risk areas, where insurance options are scarce. The dearth of coverage options has driven more high-risk homeowners to the state’s FAIR Plan — the insurer of last resort when homeowners can’t find coverage in the marketplace.

The following table compares the change in California’s average home insurance costs over time with national averages. Rates assume a dwelling coverage amount of $488,000 in California and $341,512 for the United States.

What’s next: Rates will rise less than indicated

Since 2023, home insurance costs in California have risen 16.1%. Another 16% rise in 2026 would push that cumulative increase to about 34%. But some good news remains for California homeowners.

“If we were evaluating economic factors alone, a sharper increase in California home insurance premiums would be justified,” Insurify Senior Carrier Partnerships Manager Daniel Lucas said in Insurify’s homeowner report. “However, the state’s regulatory environment and the political pressures of an election year make it unlikely that rate increases will exceed 16%.”

Commented